Quick Answer

The most common CIS return errors are failing to verify subcontractors before payment, deducting from the wrong amount (including materials or VAT), missing the 19th-of-the-month filing deadline, and not submitting nil returns. A single day late costs £100, rising to £300+ at two months. The fix is straightforward: verify every subcontractor, deduct only from labour, file on time every month, and use software that automates the calculations. With HMRC's new fraud powers arriving in April 2026, getting CIS right has never mattered more.

Table of Contents

- CIS Returns by the Numbers

- The 8 Most Common CIS Return Errors

- CIS Deduction Rates: Getting the Maths Right

- The Verification Process: Where It Goes Wrong

- CIS Penalty Structure: What Late Filing Really Costs

- Gross Payment Status: How to Keep It and How to Lose It

- CIS Rule Changes: The 2024 to 2028 Timeline

- Software That Handles CIS Automatically

- What the Experts Say on YouTube

- What the Community Thinks

- FAQ: CIS Return Errors

CIS Returns by the Numbers

The Construction Industry Scheme is one of HMRC's biggest revenue protection tools. It covers every contractor and subcontractor in the UK construction sector, and the numbers behind it tell a clear story about why getting your returns right matters.

HMRC is actively increasing its enforcement activity around CIS. In 2025, the tax authority launched a "one-to-many" letter campaign targeting contractors who had made incorrect CIS deductions, giving them 45 days to put things right. The November 2025 Budget introduced new fraud powers that come into force from April 2026, giving HMRC the ability to pursue multiple parties in a supply chain and impose 30% penalties on fraud-connected transactions.

The 8 Most Common CIS Return Errors

After analysing HMRC guidance, accountancy firm reports, and real contractor experiences, these are the eight errors that crop up most often. Each one can trigger penalties, investigations, or both.

1. Failing to Verify Subcontractors Before Payment

This is the single most common mistake. Some contractors assume that simply deducting 20% makes them compliant. It does not. You must verify every new subcontractor with HMRC before making the first payment. If you skip verification and the subcontractor should have been on a different rate, you are liable for the underpaid tax plus interest and penalties.

Verification Is Not Optional

If you cannot verify a subcontractor, the default deduction rate is 30%, not 20%. Contractors who skip this step and deduct at 20% create an immediate underpayment that HMRC will pursue.

2. Deducting From the Wrong Amount

CIS deductions apply to the labour portion only. Materials, VAT, and plant hire are excluded. Yet HMRC compliance visits regularly find contractors calculating deductions on the total invoice amount, including materials and VAT. This over-deduction short-changes the subcontractor and creates discrepancies on your return.

3. Incorrect Material Deductions

On the flip side, some subcontractors claim inflated material costs to reduce the deductible amount. HMRC specifically targets returns with unusually high material deductions relative to the type of work. Common items wrongly claimed as materials include:

- Travel costs and fuel to get to site

- Accommodation near the job

- Waste removal and skip hire

- Insurance premiums

- Tools and plant that the subcontractor owns (only hired plant qualifies)

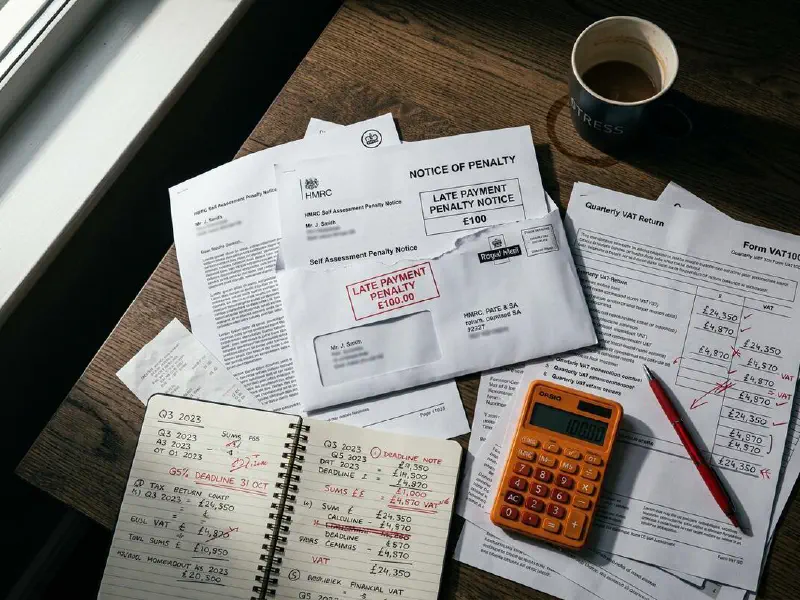

4. Missing the Filing Deadline

CIS monthly returns must be filed by the 19th of the month following the tax month end. Miss it by even one day and you are hit with a £100 penalty. Two months late adds another £200. Six months late adds £300 or 5% of the CIS deductions on the return, whichever is higher. These penalties are automatic and non-negotiable.

5. Not Submitting Nil Returns

If you made no payments to subcontractors in a given month, you still need to either file a nil return or tell HMRC you expect to be inactive for up to six months. Many contractors assume no payments means no paperwork. HMRC assumes you forgot and issues an automatic penalty.

Set Up an Inactivity Notification

If you know you will not be paying subcontractors for a few months, call the CIS helpline or use the online service to declare inactivity for up to six months. This stops the automatic penalty machine.

6. Wrong UTR or NI Number

Entering an incorrect Unique Taxpayer Reference or National Insurance number during verification means HMRC cannot match the subcontractor to their tax records. The verification fails silently, you get told to deduct at 30%, and the subcontractor loses money they should not have lost.

7. Omitting Gross Payment Status Subcontractors from Returns

A common misconception: if a subcontractor has gross payment status (0% deduction), you do not need to include them on your return. Wrong. Every payment within CIS scope must be reported on your monthly return, regardless of whether a deduction was made. Omitting gross-status subcontractors is a reporting error that HMRC will flag.

8. Getting the Scope Wrong

Not all construction work falls within CIS, and not all non-construction work falls outside it. Grey areas cause problems. Building repairs are in scope. Heating system repairs are often out of scope. Mixed contracts combining CIS and non-CIS work must have all payments brought within the scheme. Getting the scope determination wrong means either over-reporting or under-reporting, both of which attract HMRC attention.

CIS Deduction Rates: Getting the Maths Right

There are three CIS deduction rates. Applying the wrong one is one of the fastest ways to create problems with HMRC. Here is what each rate means and when it applies.

| Rate | When It Applies | What It Means |

|---|---|---|

| 20% (Standard) | Subcontractor is CIS-registered and verified | The default rate for compliant, verified subcontractors. Deducted from labour only. |

| 30% (Higher) | Subcontractor is unregistered or cannot be verified | Applied when the contractor has not verified the subcontractor, or when HMRC cannot match them in the system. |

| 0% (Gross) | Subcontractor has approved gross payment status | Subcontractor receives full payment with no deductions. Must still be reported on the monthly return. |

The Two-Step Deduction Calculation

Step 1: Take the gross payment amount and remove VAT. Step 2: Subtract verified material costs from the remaining amount. Apply the deduction rate (20% or 30%) to this final figure only. Never deduct from the total invoice including VAT and materials.

What counts as deductible labour: The labour cost itself, profit margin, subsistence, accommodation expenses, consumable stores, fuel used during construction operations, third-party plant hire, and prefabrication charges.

What is excluded from deductions: Materials directly purchased for the contract, VAT (if the subcontractor is VAT-registered), and fuel for travelling to site (as distinct from operational fuel on site).

The Verification Process: Where It Goes Wrong

Verification is the process of checking a subcontractor's details with HMRC before making any payment. It tells you which deduction rate to apply. Skipping it or doing it incorrectly is behind a huge proportion of CIS return errors.

How Verification Works

- Collect details: Get the subcontractor's full name, UTR (Unique Taxpayer Reference), and National Insurance number (or company registration number for limited companies).

- Submit to HMRC: Use the CIS online service to verify. You can also call the CIS helpline for up to 10 subcontractors per call, but telephone verifications must later be re-verified online.

- Receive the rate: HMRC tells you whether to deduct at 0%, 20%, or 30%. Record the verification number (starts with "V" followed by 10 digits).

- Apply and file: Make the payment with the correct deduction and include it on your monthly return.

When You Must Re-Verify

You need to verify a subcontractor again if they have not appeared on any of your CIS returns within the current or previous two tax years, or if they have changed their legal structure (for example, from sole trader to limited company). Many contractors assume a one-time verification is permanent. It is not.

Error Code 7912: Unmatched Verification

This is a common verification error. It means the details you submitted do not match HMRC's records. Double-check the UTR, NI number, and exact legal name. Even a small spelling difference will cause a mismatch. If the subcontractor recently changed their name or structure, they may need to update their records with HMRC before you can verify them.

CIS Penalty Structure: What Late Filing Really Costs

CIS penalties are automatic and escalating. There is no grace period and no warning before the first penalty hits. Here is the full breakdown of what non-compliance costs.

Late Filing Penalties

Penalties for Incorrect Returns

Beyond late filing, HMRC applies behaviour-based penalties for errors on returns:

- Careless mistakes: 15-30% of the tax due

- Deliberate mistakes: 35-70% of the tax due

- Deliberate and concealed: 50-100% of the tax due

There is also a record-keeping penalty of up to £3,000 for missing records or incorrect payment statements. Subcontractor payment and deduction statements must be issued within 14 days of the tax month's closing.

From April 2026: Fraud Penalties Get Serious

HMRC's new powers allow a 30% penalty on the business or its officers for fraud-connected transactions. Directors face personal liability alongside company penalties. The gross payment status reapplication ban jumps from 12 months to 5 years for fraud-related removals. These are the toughest CIS enforcement rules in the scheme's history.

Appeal window: You have 30 days from receiving a penalty notice to appeal. For nil return penalties, HMRC will cancel the penalty once you confirm the return was nil, but the penalty is issued automatically first, so you still need to respond.

Gross Payment Status: How to Keep It and How to Lose It

Gross payment status (GPS) lets subcontractors receive payments in full with no deductions. It is a significant cash flow advantage, but it comes with strict conditions. Losing GPS because of a preventable compliance failure is one of the most expensive mistakes a construction business can make.

The Three Qualifying Tests

1. Business Test: Your business must carry out construction operations or provide labour for construction work in the UK, and you must have a dedicated UK business bank account.

2. Turnover Test: Your net construction turnover (excluding VAT and materials) over the preceding 12 months must meet the threshold. For sole traders, that is £30,000. For partnerships and companies, it is £30,000 per relevant person (director or partner) or a minimum of £100,000 for the whole entity.

3. Compliance Test: All your tax affairs must be completely up to date. This is the test that catches most people out. Since April 2024, VAT compliance is included in this test, meaning even minor VAT issues can cost you your GPS.

How You Lose GPS

HMRC runs computer-generated reviews on a rolling programme, checking your compliance performance over the previous 12 months. Your GPS will be flagged for removal if:

- Four or more CIS300 monthly returns filed late (even 1 day late counts)

- Any CIS300, VAT, or Self Assessment return filed more than 28 days late

- Any PAYE, VAT, or CIS payment of £100+ made late

- Any Self Assessment or Corporation Tax payment more than 28 days late

- Any outstanding tax return at the date of review

- Any late National Insurance contributions (automatic refusal)

When HMRC identifies a failure, they issue a CIS 308 notice giving you 90 days' notice before removing your GPS. The first review happens 6 months after GPS is granted, with annual reviews after that.

CIS Rule Changes: The 2024 to 2028 Timeline

The CIS rules have changed significantly since 2024 and more changes are coming. Here is what has already happened and what is on the way.

VAT Added to GPS Compliance Test

VAT compliance became part of the gross payment status test. One VAT return more than 28 days late, or three late VAT returns in a 12-month period, can trigger GPS removal. Telephone GPS applications were also discontinued.

Traffic Management Brought Into CIS Scope

Traffic management services for construction operations are now within CIS. This includes temporary traffic lights, cones, signage, and preparatory road works when provided to a contractor undertaking construction operations.

Deemed Contractor Threshold Raised to £3 Million

Non-construction businesses spending over £3 million on construction operations in any rolling 12-month period must now register as deemed contractors under CIS. Personal liability for false GPS applications extended to directors and connected persons.

New HMRC Fraud Powers and Enhanced Penalties

HMRC gains power to pursue multiple parties in a supply chain. 30% penalties for fraud-connected transactions. GPS reapplication ban extended from 12 months to 5 years. Directors face personal liability alongside company penalties. HMRC expects these measures to raise £205 million in the first year alone.

MTD for Income Tax (Over £50,000)

Making Tax Digital for Income Tax Self Assessment begins for self-employed individuals and landlords with income over £50,000. CIS subcontractors above this threshold must submit quarterly updates using MTD-compliant software.

MTD Threshold Drops to £30,000

The MTD requirement extends to those earning over £30,000. More CIS subcontractors will need digital record-keeping and quarterly reporting.

MTD Threshold Drops to £20,000

The MTD requirement extends to those earning over £20,000, covering the vast majority of CIS subcontractors.

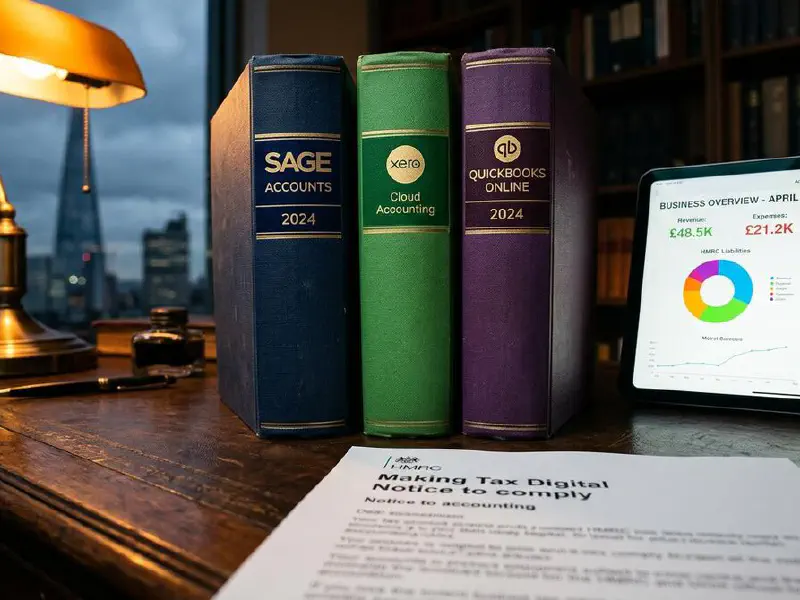

Software That Handles CIS Automatically

The right accounting software eliminates most CIS return errors by automating deduction calculations, verification, and filing. Here is how the main platforms compare for CIS compliance.

| Feature | Xero | QuickBooks | Sage | FreeAgent |

|---|---|---|---|---|

| Auto-calculate CIS deductions | Yes | Yes | Yes | Yes |

| HMRC verification built in | Yes | Yes | Yes | No |

| File CIS300 to HMRC | Yes (£5/mo add-on) | Yes (included) | Yes | No |

| Bulk email subcontractor statements | Yes | No | Yes | No |

| MTD compatible | Yes | Yes | Yes | Yes |

| Construction-specific features | CIS add-on | Built in | Full suite | Basic CIS only |

Xero calculates CIS deductions automatically on both mobile and desktop invoices. Subcontractor verification is built in, and the CIS filing add-on costs £5 per month on top of your core plan. It also bulk-emails payment and deduction statements.

QuickBooks includes CIS features at no extra cost. It handles unlimited contractors and subcontractors, auto-calculates deductions, and files directly to HMRC. For sole traders and smaller operations, this is hard to beat on value.

Sage offers the deepest construction-specific functionality, with detailed job costing alongside CIS compliance. It is better suited to larger operations that need advanced reporting.

FreeAgent includes basic CIS features but cannot file the monthly CIS300 return directly. You will need to submit it separately via HMRC's online service, which adds manual steps and room for error.

AI Is Coming to CIS Compliance

95% of accountants say technology has reduced time spent on compliance tasks. The next generation of accounting software uses AI to flag potential deduction errors before you file, automatically reconcile subcontractor payments, and predict cash flow impacts of CIS deductions. If your current setup still involves spreadsheets and manual calculations, 2026 is the year to switch.

What the Experts Say on YouTube

The 5 Biggest CIS Mistakes Construction Businesses Make

Ahmad Qayyum | Bluewater Accountants

244 views · 10:30

How To Avoid Construction Industry Scheme (CIS) Penalties

gHawk Accounting

107 views · 9:02

CIS: Everything You Need to Know About the Construction Industry Scheme

MDH Chartered Certified Accountants

16,405 views · 6:09

Construction Industry Scheme (CIS) Explained | Complete 2025-26 Guide

Pro Tax Accountant

245 views · 8:32

CIS Tax Rebates Explained! (UK)

Heelan Associates

28,930 views · 9:13

What Is the Construction Industry Scheme and How Do I Register?

HMRCgovuk

30,174 views · 5:21

The Construction Industry Scheme (CIS)

Sam Mitcham, SJCM Accountancy

6,470 views · 5:28

CIS: Paying Subcontractors Made Easy

MDH Chartered Certified Accountants

8,771 views · 4:49

What the Community Thinks

FAQ: CIS Return Errors

You receive an automatic £100 penalty. There is no grace period and no warning. If you reach two months late, another £200 is added. At six months, a further £300 or 5% of the CIS deductions on the return (whichever is higher) is applied. The filing deadline is the 19th of every month.

Yes. You must either file a nil return or notify HMRC that you expect to be inactive for up to six months. If you do nothing, HMRC assumes you forgot to file and issues an automatic penalty. You can notify inactivity via the CIS online service or by calling the CIS helpline.

You must verify a subcontractor before making any payment to them for the first time. You also need to re-verify if they have not appeared on any of your CIS returns within the current or previous two tax years, or if they have changed their legal structure (for example, sole trader to limited company).

Error code 7912 means "unmatched verification". The details you submitted to HMRC do not match their records. Double-check the subcontractor's UTR, NI number, and exact legal name. Even small spelling differences cause a mismatch. The subcontractor may need to update their details with HMRC before you can verify them.

No. CIS deductions apply to the labour portion of a payment only. Materials directly purchased by the subcontractor for the contract, VAT charges, and fuel for travelling to site are all excluded from the deduction calculation. You calculate the gross payment, remove VAT, subtract verified material costs, and apply the deduction rate to the remainder.

From April 2026, HMRC gains enhanced fraud powers allowing them to pursue multiple parties in a supply chain, impose 30% penalties for fraud-connected transactions, and extend director personal liability. The gross payment status reapplication ban jumps from 12 months to 5 years for fraud-related removals. MTD for Income Tax also starts for those earning over £50,000.