Quick Answer

The Construction Industry Scheme (CIS) requires contractors to deduct 20% tax from payments to registered subcontractors (30% if unregistered) and send it to HMRC. Both sides need to register. Subcontractors with a clean compliance record and turnover above £30,000 can apply for gross payment status to receive 0% deductions. From April 2026, monthly nil returns are mandatory again and HMRC can revoke gross payment status for five years if you're connected to supply chain fraud. Get your CIS right and it's straightforward. Get it wrong and the penalties stack up fast.

Table of Contents

- What is the Construction Industry Scheme?

- Who needs to register for CIS

- CIS deduction rates explained

- How CIS verification works

- Filing monthly CIS returns

- Gross payment status

- April 2026 changes you need to know

- Best CIS software for UK trades

- Claiming your CIS tax refund

- CIS compliance timeline

- What tradespeople are saying

- Recommended videos

- Frequently asked questions

- My verdict

What is the Construction Industry Scheme?

The Construction Industry Scheme is an HMRC tax collection system that covers payments from contractors to subcontractors in the construction industry. Under CIS, contractors deduct money from subcontractor payments and pass it directly to HMRC. These deductions count as advance payments towards the subcontractor's tax and National Insurance.

CIS has been around in various forms since 1972. The current version came into force in April 2007. The principle is simple: rather than waiting for subcontractors to pay their own tax at the end of the year, HMRC collects it at source through the contractor. It is not an additional tax. Think of it like PAYE for self-employed construction workers.

The scheme applies to all construction work in the UK, including building, demolition, alterations, repairs, decorating, and civil engineering. If you are a contractor paying subcontractors for construction work, or a subcontractor being paid for construction work, CIS applies to you. There is no minimum threshold for payments.

Who needs to register for CIS

Registration depends on which side of the payment you sit on.

Contractors must register with CIS if they pay subcontractors for construction work. This includes businesses whose main activity is not construction but who spend more than £3 million on construction in a rolling 12-month period. Property developers and housing associations often get caught by this rule. You register as a contractor by calling the HMRC CIS helpline on 0300 200 3210 or through your Government Gateway account.

Subcontractors do not legally have to register, but there is a strong financial incentive to do so. Without registration, contractors must deduct 30% from your payments instead of 20%. Over a year, that 10% difference adds up to a lot of cash sitting with HMRC instead of in your bank account. Registration takes about 15 minutes online through the Government Gateway.

You can be both a contractor and a subcontractor at the same time. A plumber who hires a tiler for a bathroom refit is acting as a contractor for that job, even if the plumber is a subcontractor on a larger project. In that scenario, you register as both.

CIS deduction rates explained

There are three CIS deduction rates, and which one applies depends entirely on the subcontractor's registration status.

| Status | Deduction rate | What it means |

|---|---|---|

| Registered subcontractor | 20% | Standard rate. Deducted from labour element only, not materials. |

| Unregistered subcontractor | 30% | Higher rate. Applies when subcontractor has not registered with HMRC for CIS. |

| Gross payment status | 0% | No deductions. Subcontractor manages their own tax payments. |

A critical detail that many contractors get wrong: CIS deductions apply only to the labour portion of a payment. If a subcontractor invoices £5,000 for labour and £2,000 for materials, the 20% deduction applies only to the £5,000 labour cost, not the full £7,000. The subcontractor receives the full £2,000 for materials plus £4,000 of the labour (£5,000 minus £1,000 CIS deduction).

Subcontractors should always separate labour and materials on their invoices. If you lump everything together, the contractor is entitled to deduct CIS from the entire payment. That is money you will get back eventually through Self Assessment, but it means less cash in your pocket month to month.

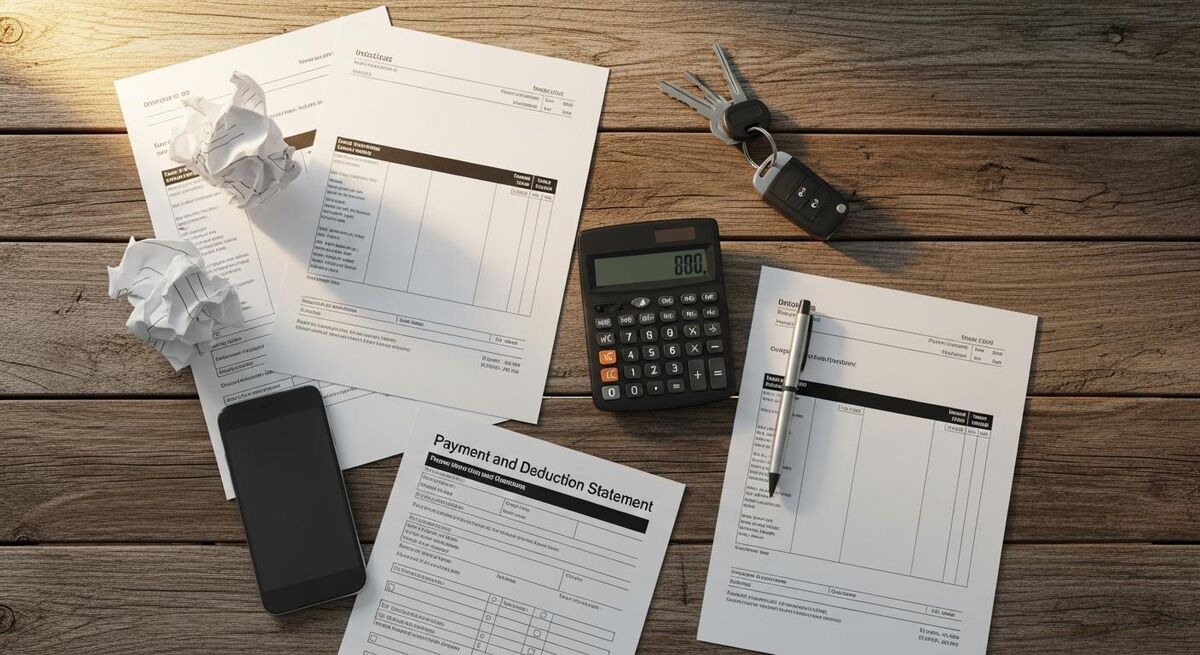

After making a deduction, the contractor must provide the subcontractor with a Payment and Deduction Statement (PDS) within 14 days. This statement is your proof that tax has been deducted and paid to HMRC. Keep every single one. You will need them when filing your Self Assessment return.

How CIS verification works

Before a contractor makes the first payment to a subcontractor, they must verify them with HMRC. This is not optional. HMRC tells the contractor which deduction rate to apply, and the contractor must use that rate.

Verification can be done online through the Government Gateway, by phone on the CIS helpline, or through CIS-compatible accounting software like Xero or Sage. The contractor needs the subcontractor's legal name, Unique Taxpayer Reference (UTR), and National Insurance number (for sole traders) or company registration number (for limited companies).

HMRC responds with one of three results: gross payment (0% deduction), net payment (20% deduction), or unmatched (30% deduction). An "unmatched" result usually means the subcontractor is not registered, or the details provided do not match HMRC records. Before deducting at 30%, double-check the details with your subcontractor, because a typo in the UTR costs them an extra 10%.

Once verified, the contractor receives a verification reference number. This must be recorded and included on monthly CIS returns. Verification lasts for the current tax year, so contractors need to re-verify subcontractors at the start of each new tax year (6 April).

Filing monthly CIS returns

Contractors must submit a monthly CIS return to HMRC by the 19th of every month following the tax month in which deductions were made. Tax months run from the 6th to the 5th, so the return covering 6 April to 5 May is due by 19 May.

The return must include: every subcontractor paid during the month, the gross amount paid, the amount of materials, the amount of CIS deductions, and the verification reference number for each subcontractor.

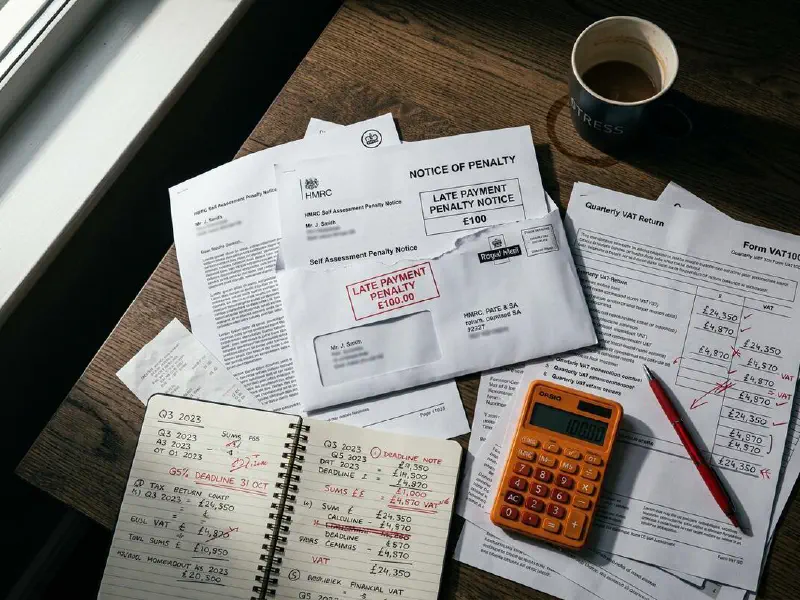

Missing the deadline triggers an automatic £100 penalty. If you are consistently late, penalties escalate. Two months late costs £200. Six months late and HMRC adds a further £300 or 5% of the CIS deductions on the return, whichever is greater. After 12 months, the same calculation applies again. These penalties are per return, so if you miss three months in a row, you face three separate penalty charges.

Returns can be submitted through HMRC's online service, through compatible software, or by a tax agent. Paper returns were abolished years ago. If you are still sending anything to HMRC by post for CIS, you need to go digital.

Gross payment status

Gross payment status (GPS) is the goal for most established subcontractors. With GPS, contractors pay you in full without any CIS deductions. You manage your own tax payments through Self Assessment. The cash flow benefit is significant.

To qualify, you must pass three tests:

Business test: You must be carrying on a business in the UK that includes construction work. HMRC looks at whether you have a business bank account, business insurance, and a genuine trade presence.

Turnover test: Your net construction turnover must exceed £30,000 per year for sole traders. For partnerships, each partner needs £30,000. For companies, the threshold is £30,000 or the company's turnover must exceed £30,000 times the number of relevant persons (directors or company secretaries who are shareholders).

Compliance test: Your tax affairs must be in order. This means all Self Assessment returns filed on time, all tax paid on time, and no outstanding tax debts. HMRC checks the last 12 months of compliance when you apply and conducts annual reviews.

You apply for GPS through your Government Gateway account or by calling the CIS helpline. Processing typically takes 6 to 8 weeks. If HMRC turns you down, they will tell you why, and you can reapply once you have fixed the issue. Under the current rules, you can reapply after one year. Under the April 2026 rules, that waiting period extends to five years for fraud-related cancellations.

April 2026 changes you need to know

HMRC introduced several significant changes to the Construction Industry Scheme from 6 April 2026. These are the biggest updates to CIS in years, and they affect both contractors and subcontractors.

Mandatory nil returns are back. Before April 2026, contractors did not need to file a return in months when they made no subcontractor payments. That exemption is gone. Every CIS-registered contractor must now file a monthly return regardless of whether any payments were made. The only way around it is to submit an inactivity request to HMRC in advance, covering up to six months of expected inactivity.

Tougher fraud sanctions. The headline change is a new "knew or should have known" test for supply chain fraud. If HMRC determines that a contractor knew, or should have known, that a subcontractor in their supply chain was connected to tax fraud, the contractor faces automatic penalties of up to 30% of the evaded tax and immediate loss of gross payment status for a minimum of five years. The Treasury expects these measures to raise £205 million in 2026/27.

Public bodies exemption. Payments to local authorities and certain public bodies acting as subcontractors are now exempt from CIS. This replaces the previous Extra Statutory Concession that covered these arrangements informally.

Best CIS software for UK trades

Managing CIS manually with spreadsheets is a recipe for errors. The right software handles verification, calculates deductions, generates Payment and Deduction Statements, and files monthly returns directly to HMRC. Here is what is available in 2026.

| Software | CIS features | Price from | Best for |

|---|---|---|---|

| Xero | Verification, deductions, returns, bulk PDS emailing | £15/month | Growing trades businesses with 5+ subcontractors |

| Sage Accounting | CIS built into Standard plan, payroll included | £30/month | Businesses needing CIS plus payroll in one package |

| QuickBooks Online | CIS included free with all QBO plans | £12/month | Sole traders and small contractors wanting simplicity |

| FreeAgent | CIS for contractors and subcontractors, MTD-ready | £14.50/month | NatWest/RBS customers (free), sole traders |

| HMRC Basic PAYE Tools | CIS returns filing only, no accounting features | Free | Contractors with very few subcontractors, on a tight budget |

Xero stands out for subcontractor management at scale. The CIS module lets you verify subcontractors directly through HMRC, auto-calculate deductions on bills, and email Payment and Deduction Statements in bulk. For businesses with a handful of subbies, QuickBooks includes CIS at no extra cost, which makes it hard to beat on value.

FreeAgent deserves a mention for sole traders, especially if you bank with NatWest, Royal Bank of Scotland, or Ulster Bank. Those customers get FreeAgent free, including full CIS and payroll functionality. That is a genuine saving of £174 per year.

HMRC's own Basic PAYE Tools is free but bare-bones. It handles CIS return filing and nothing else. No invoicing, no accounting, no bank feeds. If CIS is your only pain point and you already have accounting sorted elsewhere, it does the job.

Claiming your CIS tax refund

Most CIS-registered subcontractors overpay tax during the year. The 20% flat rate deduction rarely matches your actual tax liability once you account for business expenses, the personal allowance, and any other reliefs. The difference comes back to you through Self Assessment.

To claim a CIS refund, you file a Self Assessment tax return by the 31 January deadline following the end of the tax year. On the self-employment pages, you declare your total gross income, deduct your business expenses, and enter the total CIS deductions shown on your Payment and Deduction Statements. HMRC offsets the CIS deductions against your final tax bill. If you have overpaid, you get a refund.

Keep every Payment and Deduction Statement you receive. Without them, you cannot prove how much tax has already been deducted. If a contractor fails to provide one, chase it. You are entitled to it within 14 days of each payment.

Refunds typically arrive 4 to 8 weeks after HMRC processes your return. Filing early (the tax year ends 5 April, and you can file from 6 April) gets your refund sooner. Waiting until January means waiting until March or April for your money.

CIS compliance timeline

Before first payment

Contractor registers for CIS with HMRC. Verifies each subcontractor through Government Gateway or accounting software. Records verification reference numbers.

Each payment to a subcontractor

Contractor calculates CIS deduction on the labour element only. Pays the subcontractor the net amount. Issues a Payment and Deduction Statement within 14 days.

By the 19th of each month

Contractor submits monthly CIS return to HMRC covering the preceding tax month (6th to 5th). From April 2026, nil returns are mandatory if no payments were made.

By the 22nd of each month

Contractor pays the CIS deductions to HMRC (electronic payment deadline). The 19th deadline applies if paying by cheque.

6 April each year

New tax year starts. Re-verify all subcontractors. HMRC conducts annual compliance review for gross payment status holders.

By 31 January

Subcontractors file Self Assessment return for the previous tax year. CIS deductions are offset against the final tax bill. Overpayments are refunded.

What tradespeople are saying

Recommended videos

CIS Explained: Complete 2025-26 Guide for the UK

Pro Tax Accountant

Construction Industry Scheme (CIS) Explained

Tax Basics

Everything You Need to Know About CIS

Heelan Associates

How to Get CIS Gross Payment Status in the UK

Pro Tax Accountant

How to Claim a CIS Tax Refund in 3 Steps

Tax Rebate Services

How to Create and Submit a CIS Return

HMRC

Frequently asked questions

Legally, no. Practically, yes. If you do not register, contractors deduct 30% instead of 20% from your payments. That extra 10% sits with HMRC until you file your Self Assessment return. Register and keep that cash in your own account.

Yes. If you pay subcontractors for construction work, you are a contractor for CIS purposes, even if you are also a subcontractor on other jobs. You need to register as both and manage deductions in both directions.

Chase them. Contractors are legally required to provide a PDS within 14 days of each payment. Without it, you cannot prove tax has been deducted when filing Self Assessment. If they refuse, report it to HMRC.

No. CIS deductions apply to the labour portion only. Always itemise materials and labour separately on invoices. If you bundle them, the contractor can deduct CIS from the full amount.

Allow 6 to 8 weeks from application. You need to pass the business test, turnover test (£30,000+ for sole traders), and compliance test (clean tax record for 12 months). Apply through your Government Gateway account.

£100 immediately. £200 after two months. After six months, £300 or 5% of the CIS deductions on the return, whichever is greater. The same calculation applies again after twelve months. These are per return, not per year. Details in our MTD penalties guide.

The nil return requirement and fraud sanctions primarily affect contractors. But subcontractors with gross payment status should pay attention. If your contractor loses GPS because of supply chain fraud, that disruption flows down to you. Make sure the contractors you work with are compliant.

My verdict

I have seen too many tradespeople treat CIS as someone else's problem. It is not. Whether you are a contractor or subcontractor, the scheme touches every payment you make or receive for construction work. The basics are straightforward: register, verify, deduct, file, repeat. Get decent software, separate your labour and materials on every invoice, and keep your Payment and Deduction Statements. The April 2026 changes add an extra layer of responsibility for contractors around supply chain due diligence, but the fundamentals have not changed. If you are a subcontractor with a clean record and decent turnover, apply for gross payment status. The cash flow benefit is real. And if you are still managing CIS on spreadsheets, it is time to move on. The cost of a compliance mistake is always higher than the cost of the software that prevents it.

Stay on top of your CIS obligations

TrainAR Academy publishes practical guides on tax compliance, CIS, MTD, and business operations for UK trades professionals. Bookmark the site and check back for updates as HMRC rules evolve.

Visit TrainAR Academy